Why Inflation is Less Harmful Than You May Think

Written by Godfrey Yu

One of the big topics of conversation in recent months has been inflation. A generation of Canadians built their retirement plans on the Bank of Canada’s 2% inflation-control target. Yet, in December of 2022, prices continued to grow at 6.3%—dropping below market expectations, but still remaining well above the central bank’s threshold.

Investors are facing “sticker shock” on their grocery bills or at the gas station, and this sometimes leads to anxious questions about their investments. How is inflation impacting my future? Am I still on track for retirement? Do I have enough for my children’s education? In such times, it can be hard to see the forest for the trees.

But despite the pain that Canadians may be experiencing in their pocketbooks, temporary setbacks to wealth planning are often muted over the long term. Inflation, along with the rate of return, will have its ups and downs—and, truthfully, some years are better than others. For this reason, wealth planners will typically look at a larger sample size, around 20 to 30 years, or even longer, depending on life expectancy.

Also, the current spike in inflation is an anomaly. Over a broader timeframe, the BoC’s 2% target is a good representation of the average rate in Canada and acts as an appropriate guideline for long-term projections. Moreover, the BoC’s aggressive rate hikes are starting to work their way into the financial system, and should reduce price growth going forward.

Staying the Course

It’s our belief that every good financial plan starts with a discussion about clients’ specific goals. Only by understanding each unique situation—their varying stages of life and personal circumstances—can we create an investment roadmap to reach them and monitor progress along the way. This focus does not change when markets are volatile.

For instance, let’s consider a client who reviews her portfolio and sees that it is down 10%. If she has invested $2 million, that represents a $200,000 decrease. In this case, the amount of money can seem a lot bigger than the rate of change—and it can feel uncomfortable. What can be helpful here is to put everything into historical context.

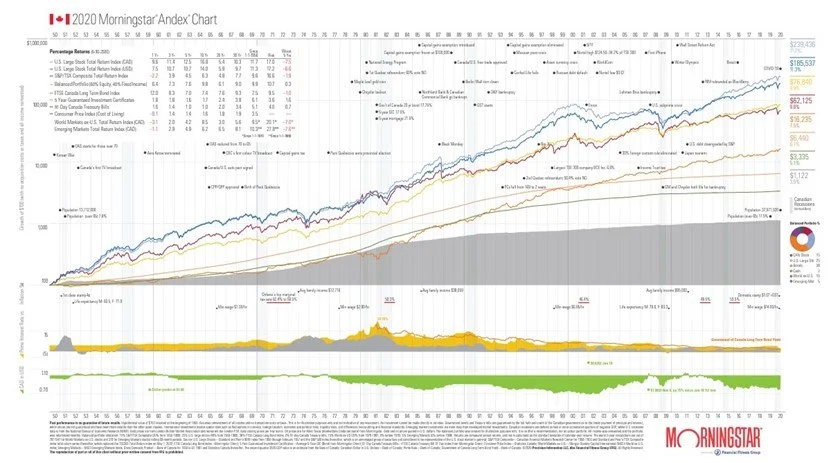

The following Andex Chart tracks the hypothetical performance of $100 invested at the beginning of 1950, outlining the various political, economic and social that markets eventually overcame to reach new heights.

Say the client was born in 1960 and started investing in her early 30s, she would have already lived through four market challenges of equal, or greater, volatility. A recession in the early ‘80s, a Dot-Com Bubble in 2000, the 2008 Global Financial Crisis, and, most recently, the COVID-19 pandemic.

As data shows, by staying invested from then until now, she would have seen a series of market recoveries and ultimately be wealthier for it. The same principle applies today—for near-retirees and the next generation of investors alike. Whether you’ve lived through multiple crises, or are experiencing your first downturn, in unsteady markets we always go back to the financial plan rather than looking at the short-term volatility.

Historically, this tends to be a winning strategy. Investors who sell when asset prices are depressed may find it difficult to correctly time markets on the rebound, thus impairing their long-term performance.

This is why, at JCIC, our investment portfolios focus on strong, stable companies we trust to compound growth reliably over time. By thinking in terms of years, rather than weeks or months, we can withstand major market movements and smooth out the impacts of world events to meet our clients’ true objectives—to live a good life.

NEWSLETTER

Disclosure

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of JCIC Asset Management, its editors and contributors, and may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice, solicitation and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your Relationship Manager prior to making any investments, including whether any investment is suitable for your specific needs.