2024 Performance Report

We are pleased to announce that JCIC achieved strong returns for our clients in 2024. This report contains detailed information about our portfolios’ performance and explains some of our successful strategies. If you would like clarification on any of this information please contact one of our relationship managers.

Kai Lam, Chief Investment Officer

Our flagship fund, the JCIC Balanced Fund, delivered a return of 19.0%, while the JCIC Equity Fund saw a return of 24.0%. Additionally, we offer specialized segregated equity models, which performed exceptionally well: our US Equity model returned 46.9% (compared to the S&P 500’s total return of 36.0% in CAD), our Canadian Equity model yielded a return of 29.1% (versus the TSX total return of 21.6%), and our International Equity model achieved a return of 14.6% (compared to the MSCI EAFE’s total return of 13.5% in CAD) for 2024.

Among the top-performing stocks in the US were Amazon.com (+57.5%), JPMorgan Chase & Co. (+57.4%), Alphabet Inc. (+47.9%), and Apple Inc. (+42.5%). In Canada, leading stocks included Agnico Eagle Mines Ltd. (+58.5%), Brookfield Asset Management (+51.7%), and Dollarama Inc. (+47.3%). From international markets, Rheinmetall AG (+118%) and Taiwan Semiconductor (+110%) were standout performers.

All figures are quoted in Canadian dollars.

What Happened in 2024?

After a strong performance in 2023, we entered 2024 with a more cautious yet constructive outlook. We recognized the risk of a mild recession in Canada and Europe and anticipated a soft landing in the United States. The recession risk stemmed from the delayed effects of interest rate hikes and high consumer debt levels. Conversely, the outlook for a soft landing in the US was influenced by a unique mortgage market, where consumers secured 30-year mortgages at low rates before the increase in rates. As a result, the US economy is less sensitive to interest rate hikes than other markets.

However, a shallow recession did not materialize, as illustrated in Figure 1. Throughout 2024, global GDP (Gross Domestic Product) estimates generally improved, with this growth outlook particularly pronounced in the United States.

Figure 1.

In addition, despite the rising growth expectations, inflation trended down (Figure 2), which allowed global central banks to cut interest rates (Figure 3).

Figure 2.

Figure 3.

Broad Economic Trends

The combination of improving economic growth, lower inflation, and interest rate cuts contributed to strong performance in the equity markets in 2024.

In the first half of the year, fixed-income investments struggled but achieved positive returns. Canadian fixed-income performed better, benefiting from more significant rate cuts and weaker economic conditions compared to the US. In contrast, US fixed-income returns were more subdued, as rates decreased slower due to stronger economic growth, a tighter labour market, and persistent inflation.

Figure 4.

What do we expect for 2025?

Growth is expected to improve in 2025, aided by interest rate cuts seen globally. While the impact of these cuts may not be as significant in the US, the new Trump administration could bring other potential benefits. Following Trump's victory in the US Presidential election, the US equity market rallied due to anticipated tax cuts and deregulation that could further stimulate growth. This environment is likely to support companies in achieving earnings growth. However, some uncertainties could introduce volatility to the markets.

In equities, valuations in the US have increased to relatively high levels, with significant growth observed during 2024 (see Figure 5). Given these elevated valuations, it would not be surprising to see market volatility at the start of the year. Potential catalysts for this volatility include uncertainty surrounding President-elect Trump's policy implementations, such as tariffs, protectionism, and possible retaliatory actions from other countries and regions, including China, Canada, Mexico, and Europe.

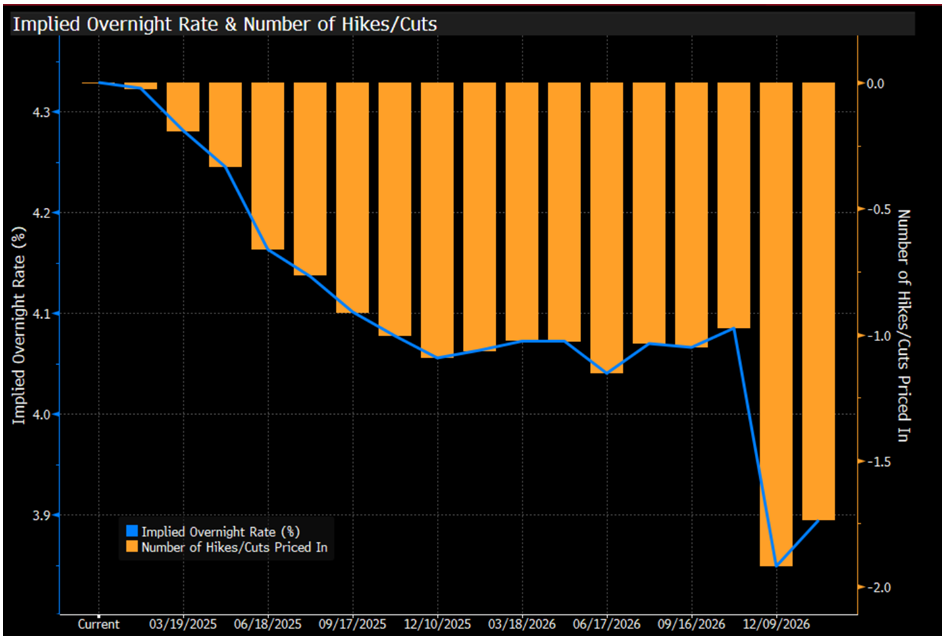

Another risk factor to consider is the rise in US long-term bond yields. As shown in Figure 6, the 10-year US government yield has increased from a low of 3.6% to its current rate of 4.8%. This rise reflects a more optimistic growth outlook for the US but also brings inflationary risks and decreased expectations for further interest rate cuts. Since the US Federal Reserve has cut rates by 100 basis points since September, the futures market is pricing in no additional rate cuts in the US until the second half of 2025 (see Figure 7). While these factors contribute to market jitters, they also create opportunities, and we maintain a positive outlook for the market throughout the year.

Figure 5.

Figure 6.

Figure 7.

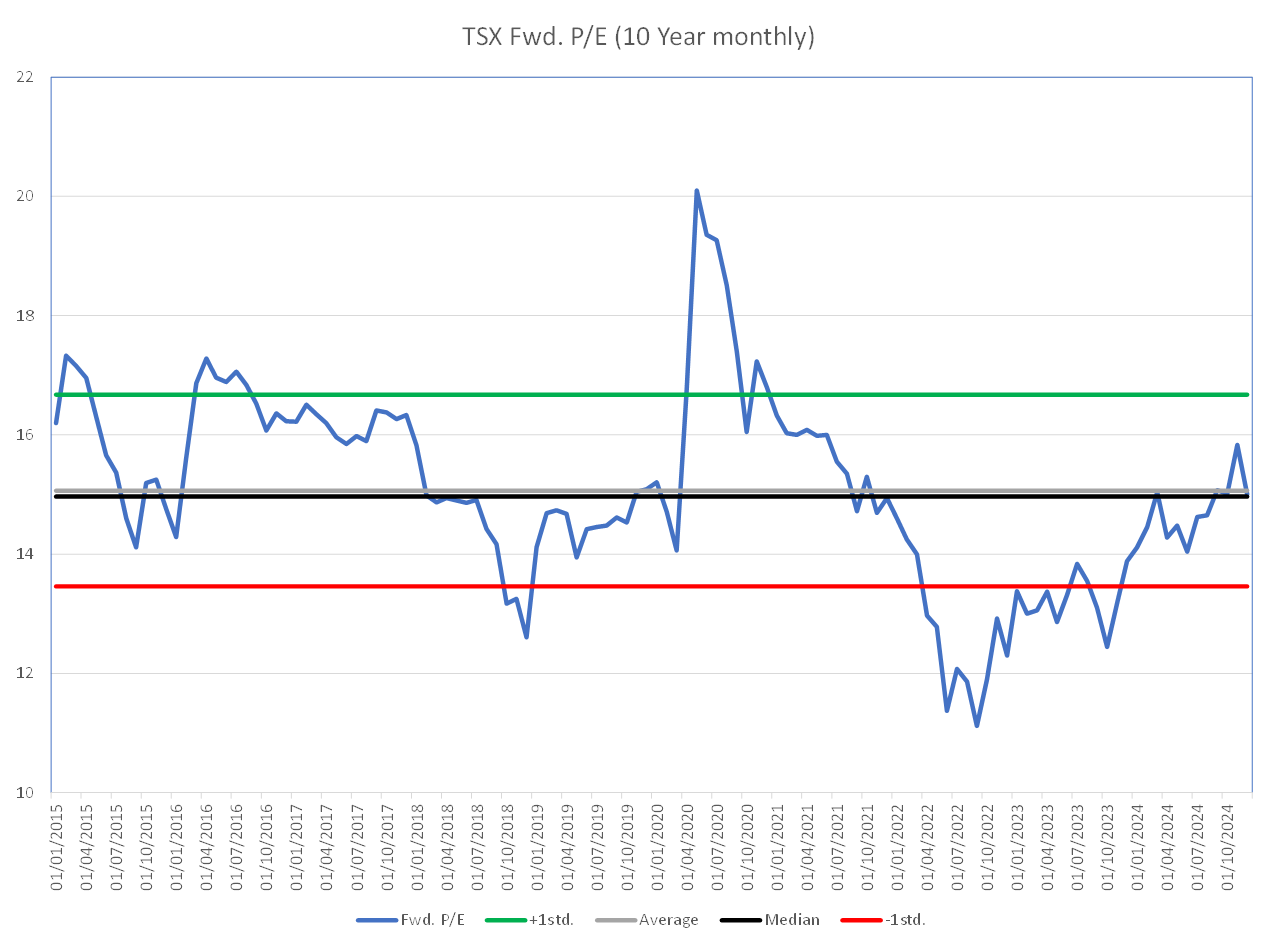

Valuation is not universally high. When we examine the equally weighted S&P 500, we find that valuations are more reasonable because they are not influenced by the Magnificent Seven mega-cap stocks (see Figure 8). The current valuation in the Canadian markets (see Figure 9) is only at the 10-year historical forward Price/Earnings ratio. Looking at international markets (see Figure 10), the MSCI EAFE index is well below its average valuation levels. This significant international discount may present a substantial opportunity, particularly if the relative economic performance of non-North American markets begins to improve.

Figure 8.

Figure 9.

Figure 10.

Source for all charts: Bloomberg

Final Thoughts

Despite the potential for various challenges, we maintain a positive outlook for 2025. We anticipate that growth will improve compared to 2024, largely due to the effects of lower interest rates. Earnings growth will play a more significant role in driving market performance than valuation expansion.

The beginning of Trump's presidency may introduce uncertainty regarding government policies, tariffs, and the international political landscape. We will closely monitor the implementation of his policies.

Our core investment strategy remains the same; however, we will adjust it to navigate the evolving market environment and seize emerging opportunities.

If you have questions about any of this information, please don’t hesitate to reach out to us:

Disclosure:

Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of JCIC Asset Management, its editors and contributors, and may change without notice. Any views or opinions expressed in the newsletter may not reflect those of the firm as a whole. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. No recommendation or advice is being given as to whether any investment is suitable for a particular investor or a group of investors. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. We strongly advise you to discuss your investment options with your Relationship Manager prior to making any investments, including whether any investment is suitable for your specific needs.

The information provided in our newsletter is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. JCIC Asset Management reserves all rights to the content of this newsletter.

* Performance percentages stated are gross of fees.